Webinar

The identity gap: Where marketing feels effective and where it breaks down

Learn more

Earth Day is coming up, and with it a slew of brands coming through with cause-related marketing, hoping to appeal to green product buyers. And cause marketing has a real impact on a brand’s bottom line:

But consumers are getting more particular and savvy about the brands they choose to buy from—they won't stand for anything that feels inauthentic or "greenwashed." Understanding this audience is more important than ever, but how do you actually quantify the “green market”?

Using Epsilon’s media planning and clean room platform, which aggregates Epsilon’s CORE ID data at scale for granular consumer insight for media planning purposes (without any consumer-level information), we took a peek at natural market shoppers (in partnership with Publicis Commerce) to better understand their larger demographics and identify prevalent attributes to help cause marketers better connect with this group.

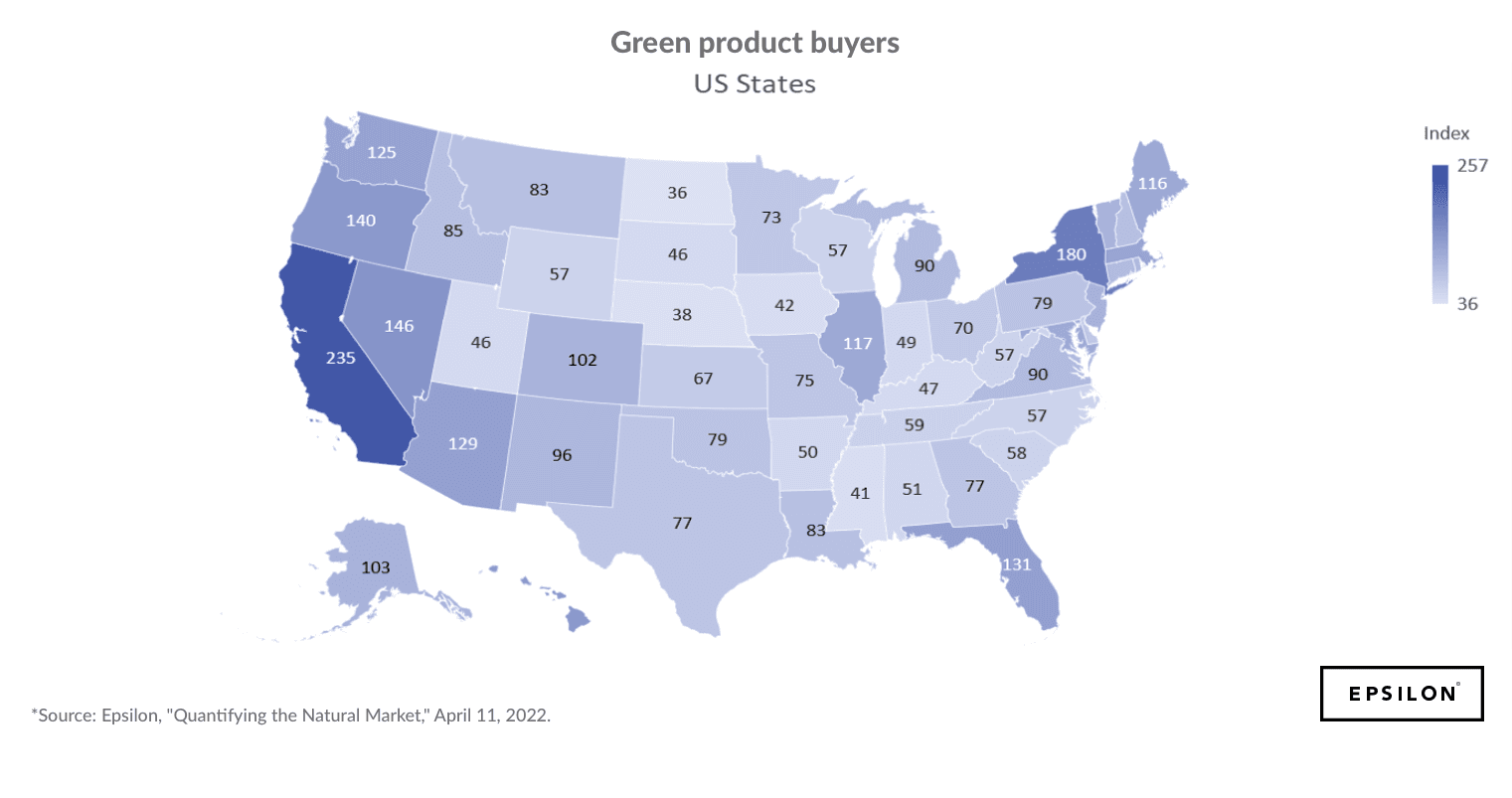

In our data, we use a propensity model to score shoppers based on who has/hasn’t purchased “green” products; this group of “green shoppers” is the top 10% of all CORE IDs that are likely to buy green, essentially the people who buy green the most.

When looking at buyers’ potential to be green shoppers across the US, we see very few states that actually over-index for this group. The usual suspects show up, like California, Oregon, Washington and New York, but we also see states like Arizona, Nevada and Florida as areas with more than average green-product buyers.

When analyzing this audience segment, we see a few key themes emerging:

But there are many and different ways that someone could be a “green” buyer, so it’s also important to look into specific product categories that have clear options for consumers to select a “natural” product, and from there, further investigate who is more likely to buy a regular natural product versus a more premium option.

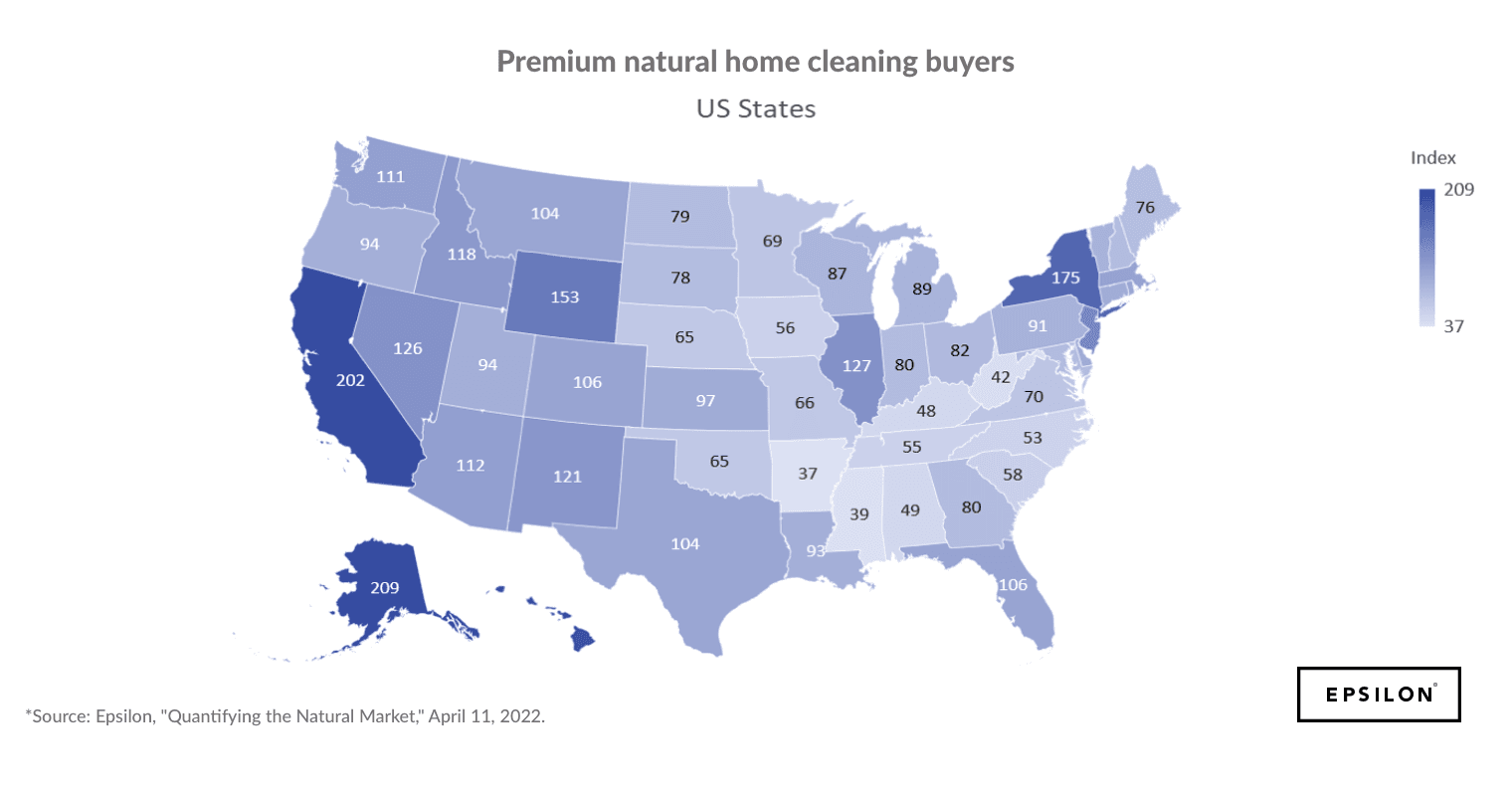

If we dig a little bit deeper, we can look into how people buy across regular natural products versus “premium” natural products (think of the difference between buying Mrs. Meyers versus its premium sister brand, Caldrea). Those classified as premium buyers are defined as people who are “willing to pay a premium price for a natural product.”

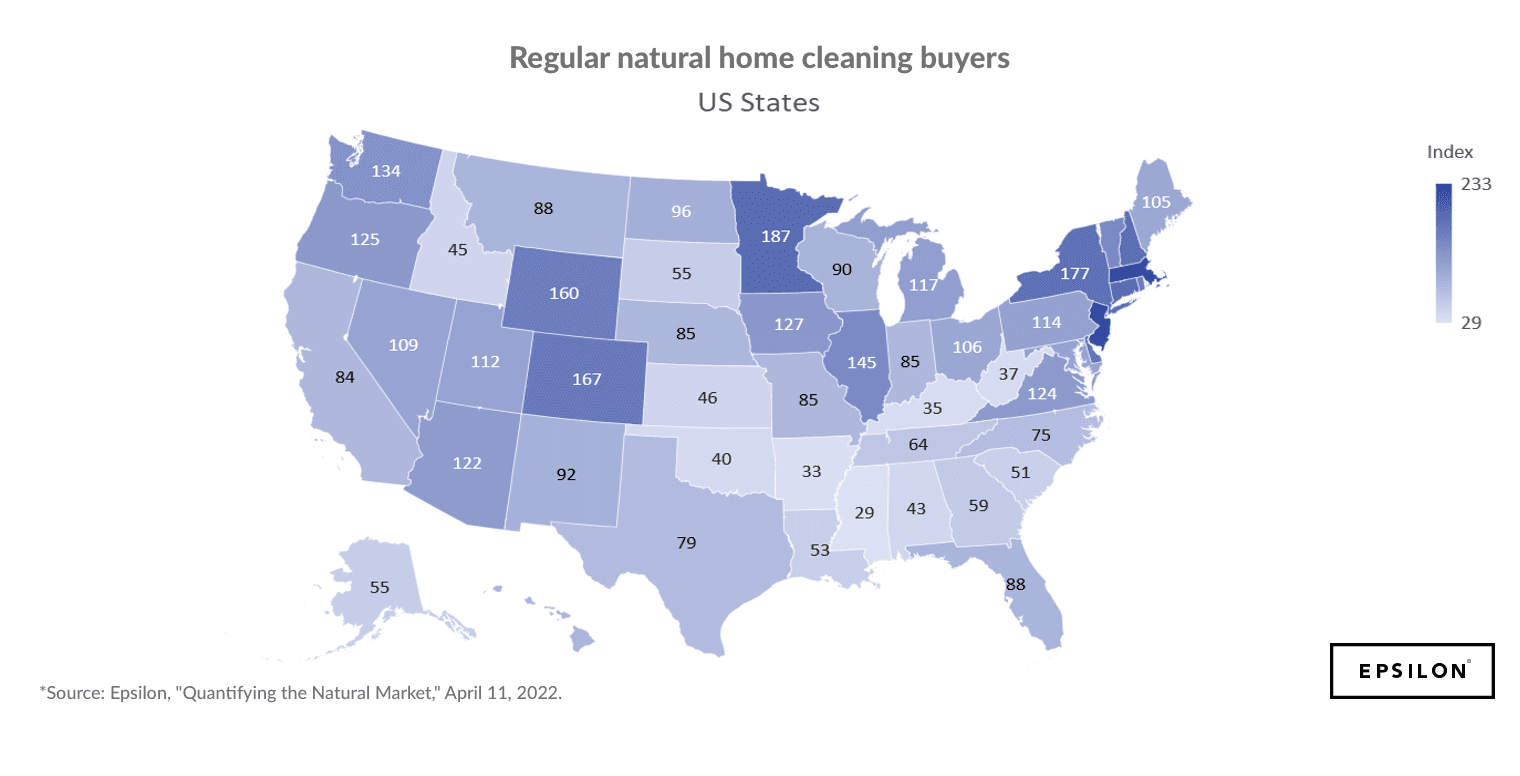

Here’s a look at how regular natural home cleaner buyers compare to premium home cleaner buyers:

As you can see from the maps overlaid with the natural home cleaner data, some states are great markets for both premium and regular natural home cleaning products while others are better for just one or the other:

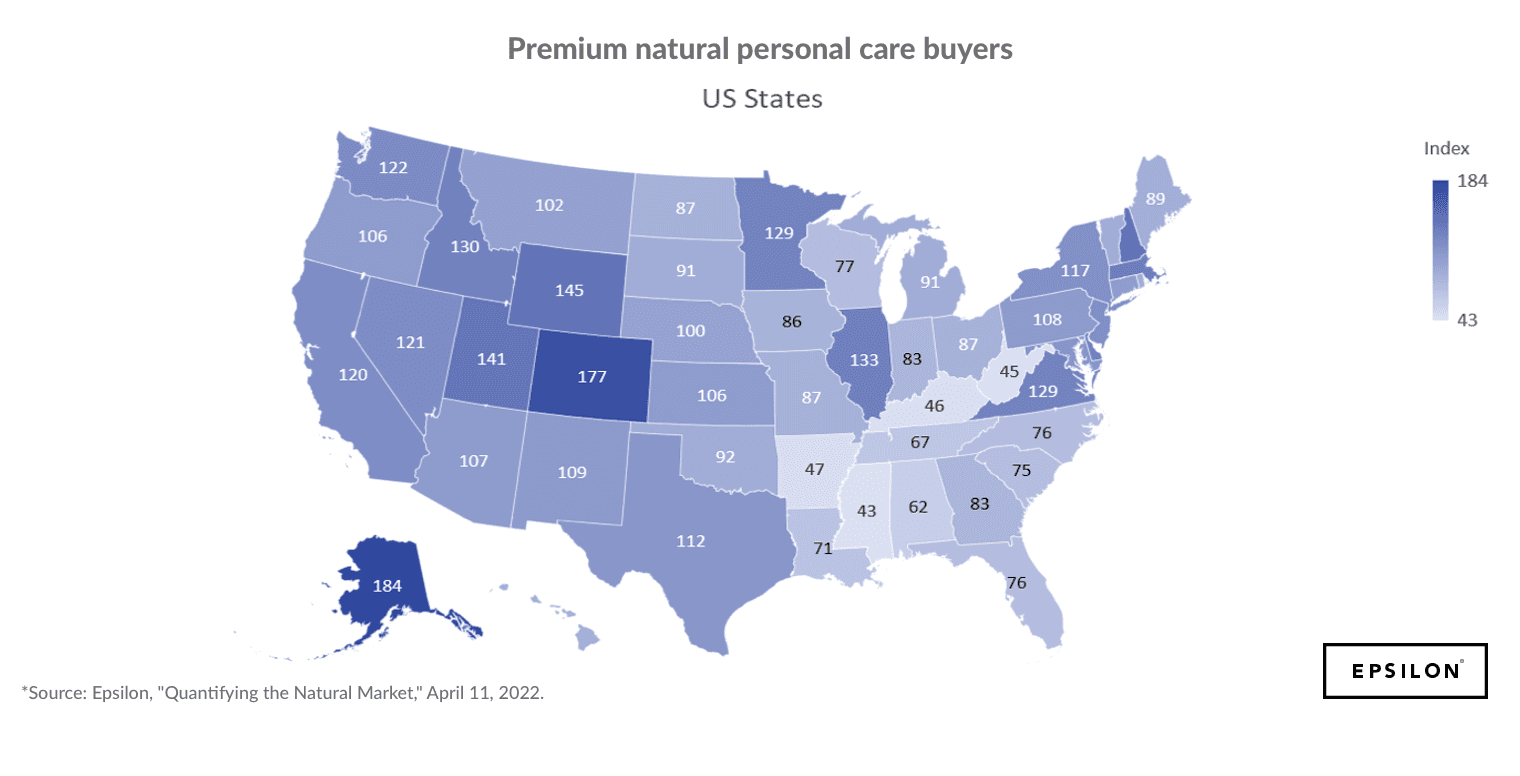

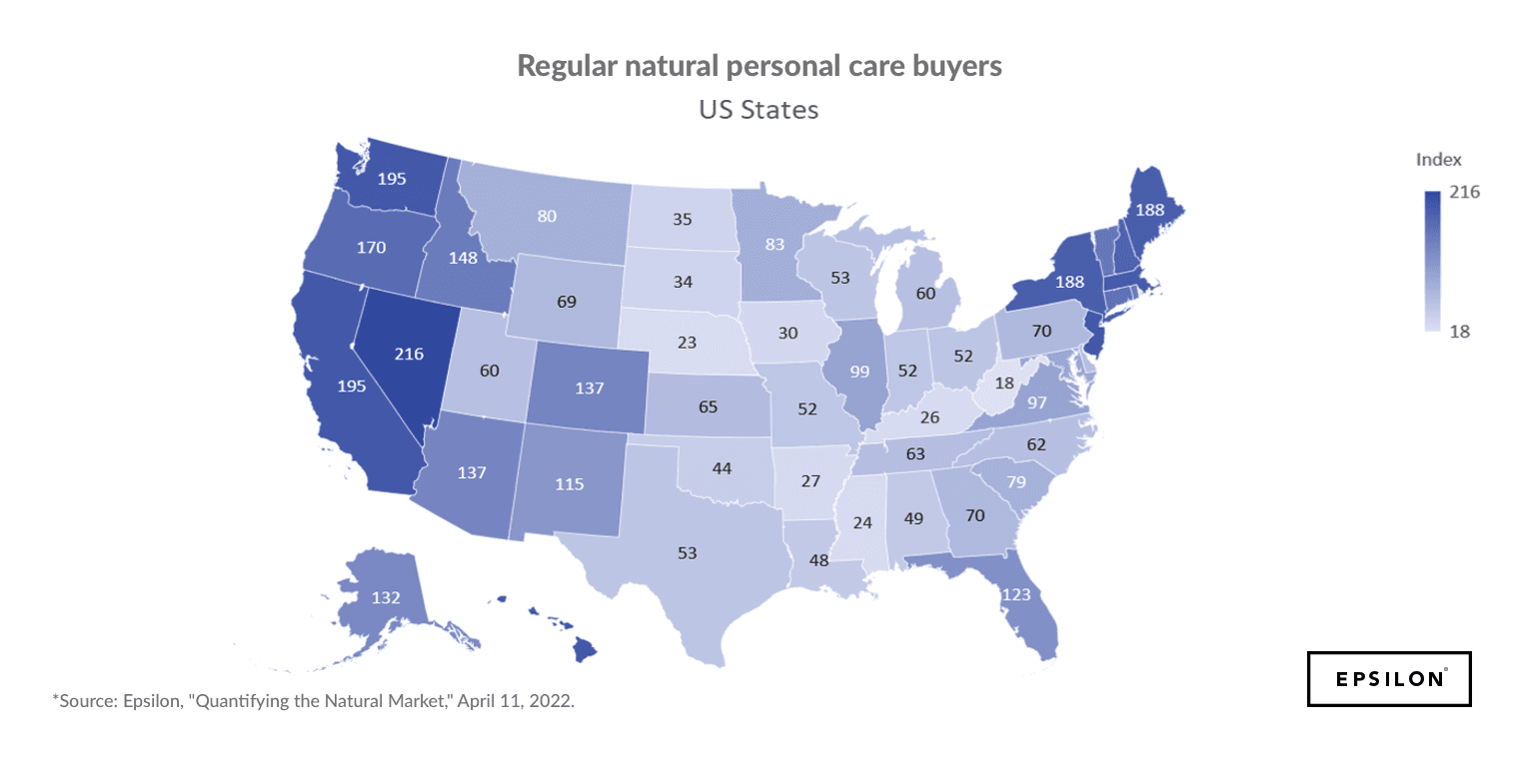

The same is true when we look at regular natural personal care versus premium natural personal care:

It’s worth noting that premium personal care buyers are also highly likely to be premium natural home cleaner and premium natural laundry product buyers (top 10% for each). Other high percentile traits for this group are that they’re avid book readers, Target enthusiasts, restaurant loyalty card customers, home gym owners and live concert attendees.

Again, we see some states that over-index for both categories. but others that over-index for one or the other:

Both groups over-index as female, which isn’t surprising, but there are a few other demographic differences worth highlighting:

Regular Natural Personal Care Buyers Regular Natural Personal Care Buyers Age? 25-44 or 65-74 25-44 Children? Yes, ages 1-2 Yes, ages 1-6 Education? College education Graduated college and graduate school Other attributes: Purchased health & wellness vitamins and supplements in the past 6 months, heavy label reader, not a DIY-er Browsed private schools, luxury & upscale shoppers, browsed grilling, electronics, fashion, politics and home cooking topics

This information helps to connect the dots across who is actually buying natural, green products today and what they care about. But just about any brand today can’t ignore how cause-related marketing impacts their brand and community.

Participating in awareness holidays, like Earth Day, does have an impact. Old Navy is a great cause marketing example: For World Water Day in March and then Earth Day in April last year, the clothing brand launched a multi-pronged initiative to showcase their green future and commitment to young changemakers. As part of their #ImagineABetterFuture campaign, they showcased how they’re investing in the next generation and their commitment to climate change.

First, they pledged to have 85% of the fibers used in their clothing to come from sustainable sources by 2025, a fairly aggressive and nearer-term goal for such a large brand. Then they named Ryan Hickman, an 11-year-old, as the brand’s new head of “fun-cycling” and invested in Hickman’s nonprofit organization dedicated to recycling awareness. They also selected 51 (in honor of the 51st Earth Day) environmentally focused GoFundMe fundraisers, which were all led by youth activists. And to top it off, they eliminated all plastic shopping bags at its stores in the U.S. and Canada.

We know that consumers can see through inauthentic, greenwashing initiatives, so how do you ensure your brand doesn’t fall into that category?

Cause-related marketing is important for all brands, whether they’re simply looking to connect with a cause-specific buying group or building their holistic cause-related marketing strategy.

Interested in learning more about how Epsilon can with your loyalty strategy and consumer insights? Check out our loyalty marketing solutions and data platforms.