Blog

ROAS vs incremental ROAS: which metric actually proves your media is working

Learn more

Customer acquisition has never been more competitive. With marketing budgets under pressure across Europe, brands can no longer rely on broad reach and last-click attribution to justify spend. This guide covers what an effective customer acquisition strategy looks like in 2026, and how European brands are building smarter, more measurable approaches to sustainable growth.

Customer acquisition is the process of attracting and converting new customers. It sounds straightforward, but doing it efficiently, at scale, and in a way that can be measured and optimised is where most brands struggle.

For EMEA marketers, the challenge has deepened. The open web is fragmenting, third-party cookie deprecation has disrupted traditional targeting, and consumers across the UK, France, Germany and beyond expect increasingly personalised experiences. Meanwhile, GDPR has raised the bar for how data can be used, and the brands navigating this well are those treating first-party data as a strategic asset rather than a compliance obligation.

Customer acquisition cost (CAC), the total spend required to bring in one new customer, is the central metric to manage. A healthy benchmark is a 3:1 ratio of customer lifetime value (LTV) to CAC. But for that ratio to mean anything, you first need to measure both accurately.

Brands that can match in-store and online purchase behaviour to individual customer identities, rather than treating each channel as a separate silo, consistently achieve lower CAC and higher LTV-to-CAC ratios.

Every customer acquisition strategy maps to a journey with three core stages. Understanding where your prospects are at any given moment shapes both the channels you use and how you message them.

Stage 01 Discovery: A prospect identifies a need and evaluates options, often via search, social, or a retailer's website. This is where brand awareness and educational content do the heavy lifting.

Stage 02 Consideration: The prospect narrows their shortlist and engages more actively, reading reviews, comparing pricing, or responding to retargeting. Personalisation and proof points become critical here.

Stage 03 Conversion: The prospect becomes a customer. Conversion is not the endpoint; it is where acquisition cost is validated and the retention journey begins.

Start with a clear ideal customer profile, covering not just demographic data but behavioural patterns and purchase signals. Brands operating retail media networks across UK, French and German retailers, for example, can use first-party transaction data to build audience models based on actual shopper behaviour rather than modelled proxies.

In a post-cookie world across Europe, the quality of your own customer data is your most valuable acquisition asset. Establish what you have, identify duplication, resolve identities across touchpoints (web, app and in-store) and understand the gaps. Many EMEA brands are surprised to discover they hold far more useful data than they are actively using.

No single channel delivers an acquisition strategy on its own. Email, display, search, connected TV, retail media and direct mail each play a role at different funnel stages. The critical factor is how these channels connect, both in messaging continuity and in measurement. Fragmented channel execution leads to fragmented data and inflated CAC.

Define what you are measuring before launch: cost per acquisition (CPA), return on ad spend (ROAS), new customer revenue, and the LTV-to-CAC ratio. Where possible, measure back to transactions rather than click-through rates, which have limited correlation with real business outcomes.

Acquisition strategy is not a set-and-forget exercise. Build a testing framework from day one, testing creative, audience segments, channel mix and landing page experience. Identify where prospects drop out of the funnel and address root causes rather than symptoms.

Strategy is one thing. What it looks like in practice across a major European retail brand is another. Decathlon's experience illustrates how several of the principles above come together into a coherent, measurable acquisition programme.

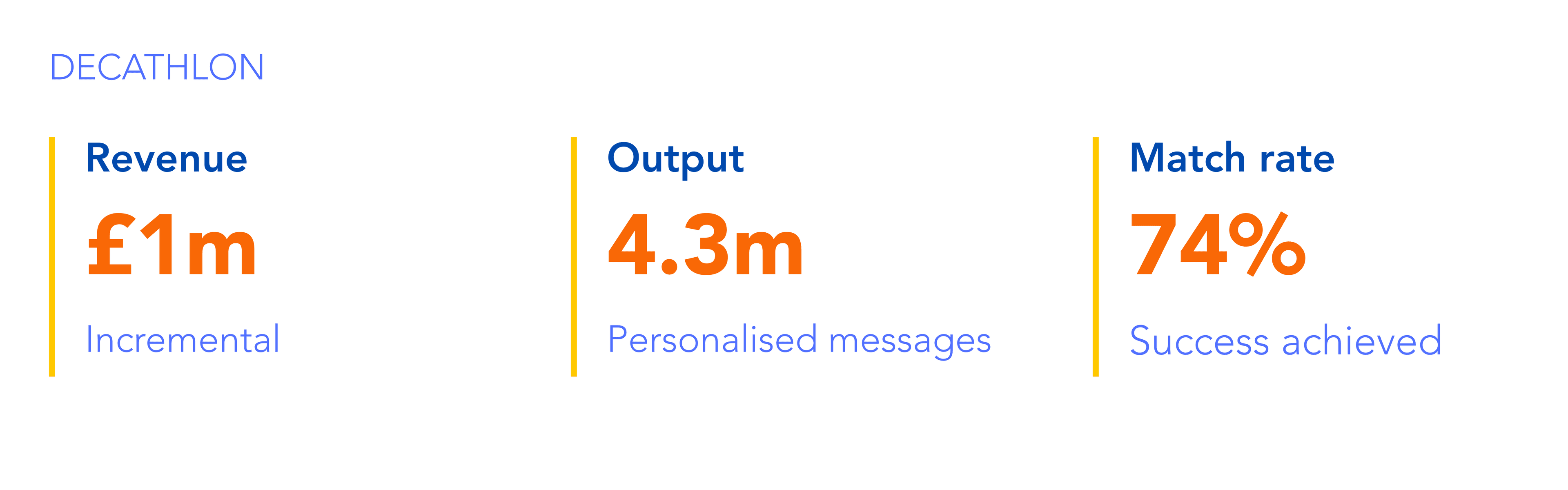

As post-COVID buying habits shifted and consumers returned to physical retail, Decathlon faced a familiar challenge: customers who had transacted online were becoming harder to identify and reach as their behaviour changed. With a product range spanning 70 sports categories, the brand also needed to go beyond retaining existing buyers and actively acquire new customers across each of them.

Decathlon worked with Epsilon to build a single customer view, consolidating fragmented data into unified, person-level profiles. From there, the team introduced automation to build target audiences faster, get campaigns live more quickly, and deploy data-driven dynamic creative at scale. The result was more personalised acquisition communications delivered to the right people, across the right categories, at the right time.

One of the most significant outcomes was the match rate. By onboarding and enriching the Decathlon customer database, Epsilon achieved a 74% match rate, well above what the brand had anticipated, and directly enabling more effective customer acquisition activity from day one.

Using a single customer view to drive customer acquisition across 70 sports categories.

The Decathlon example highlights something that applies across most EMEA acquisition programmes: the measurement model matters as much as the media strategy. Traditional last-click attribution credits only the final touchpoint before conversion, typically paid search or retargeting, while ignoring the awareness-building activity that initiated the journey. This systematically overvalues bottom-funnel tactics and undervalues the channels doing the harder work of generating new demand.

What changed for Decathlon was a shift from campaign-level reporting to business metrics. Rather than measuring impressions and clicks, the team measured incremental revenue and return on ad spend against actual purchase behaviour. That shift in measurement is what gave the brand confidence to scale up investment, knowing the returns were real and attributable.

Brands that measure acquisition outcomes at the transaction level, rather than the click level, consistently find their channel mix and true CAC look significantly different from what standard attribution reports show.

Marketers operating across European markets face a set of constraints and opportunities that do not apply in the same way elsewhere:

Customer acquisition is not a standalone objective. The economics only work when new customers are retained and developed over time. A low CAC achieved through high-volume, low-quality acquisition, targeting easy audiences who quickly churn, is ultimately worse than a higher CAC applied to customers with strong lifetime value trajectories.

The brands building durable acquisition programmes in EMEA are those connecting acquisition data to retention strategy from day one, using the same customer identity and transaction data that drives targeting to also measure loyalty, reactivation and CLV growth over time. Acquisition and retention are not separate workstreams competing for budget. They are two stages of the same customer value journey.

Epsilon works with leading European brands to build acquisition programmes grounded in first-party data, identity resolution and transaction-level measurement.